What is the Modern Portfolio Theory

The Modern Portfolio Theory, or Modern Portfolio Management Theory, is a strategy for building portfolios with financial assets developed by Nobel Prize winner Harry Markowitz. MPT, Modern Portfolio Theory in its English name and acronym, was published in March 1952 in The Journal of Finance, under the title Portfolio Selection, and analyzes the portfolio from a rational point of view based on the efficient use of risk, or as we will see below, based on volatility (as a risk proxy).

In this model, Markowitz did not consider each asset in isolation but included in a portfolio of assets. And, for that, it used statistical concepts such as the normal distribution to explain the distribution of the returns of the assets, namely using the average of the returns, the variance of the returns in relation to the average and the correlations between the returns of the different assets. One of the main characteristics of this model is precisely related to the correlation: whenever the correlation is less than 1 (one), the assets have the potential for diversification and, therefore, for risk reduction.

The Modern Portfolio Theory establishes that investment opportunities can be evaluated by using expected returns as a measure of reward and the variance of returns as a measure of risk.

Markowitz based his work on the assumptions that the market is efficient, more reliable than the individual investor's intuitions, and on the need for diversification to distribute investments across different asset classes.

Based on this theory, several models were developed, such as the mean-variance optimisation and the CAPM (capital asset pricing model), introduced by William Sharpe in 1964. The CAPM, and all studies and research involved in the development of the model, brought terms such as beta, alpha and systematic and non-systematic risk into the financial lexicon (concepts to be analyzed in the next article). These concepts, in addition to the risk-free asset, the market risk premium and diversification, have become essential elements in the valuation of assets and in the construction of investment portfolios.

Some topics from Markowitz's work

The work begins with the phrases “THE PROCESS OF SELECTING a portfolio may be divided into two stages. The first stage starts with observation and experience and ends with beliefs about the future performances of available securities. The second stage starts with the relevant beliefs about future performances and ends with the choice of portfolio.”

Markowitz argues that portfolios must optimize the expected return in relation to volatility and suggests a threshold that he called the "efficient frontier". The efficient frontier is the set of investment portfolios that are expected to produce the highest returns considering a given level of risk. A portfolio is said to be efficient if there is no other portfolio that offers higher returns for a lesser or equal amount of risk.

Also, consider 2 rules:

- The investor maximizes (or should maximize) the expected return, that is, maximizes the future value of discounted returns;

- The investor considers (or should consider) the expected return as something desirable and the variance of returns as something undesirable.

Regarding diversification, the author notes, "Diversification is both observed and sensible; a rule of behaviour which does not imply the superiority of diversification must be rejected both as a hypothesis and as a maxim".

An example of an MPT-based portfolio:

- 40% equity (25% large-cap stocks and 15% small and mid-cap stocks);

- 50% bonds (25% government bonds and 20% corporate bonds and 5% high yield bonds);

- 5% in raw materials;

- 5% in gold.

Main advantages and benefits

Markowitz's work is still the preeminent paradigm for analyzing and applying risk and return principles in portfolio management and in using diversification to help investors avoid disastrous outcomes.

The examples of inefficient and wrong portfolios from the diversification point of view are the best way to demonstrate the benefits of this systematic process. An efficient and diversified portfolio produces more returns per unit of assumed volatility. It is the maximization of risk-adjusted return, considering that the investor:

- It is risk-averse – investors are more comfortable with less risk;

- Sets rational expectations

- And practice asset integration

MPT seeks to eliminate the specific risk of an investment portfolio, the risk associated with the individual asset and its own characteristics. In striving for a diversified investment portfolio, Markowitz argues that it is possible to eliminate the specific component of risk, keeping only the systematic component, that is, market risk. Therefore, the theory assumes that the investor will consider how much the risk of an asset can impact his entire portfolio.

With a well-balanced, weighted and diversified portfolio, and according to MPT, if some of the assets depreciate due to market conditions, others will rise in compensation.

So, in summary, the main advantages of the strategy are:

- The diversification process;

- Reducing the level of volatility;

- The creation of efficient, balanced and long-term portfolios.

Markowitz's central objective was to take a portfolio as a whole. The portfolio, in an integrated way, is less volatile than the sum total of its parts.

Disadvantages for investors

Some investors and other market participants claim that the poor results of optimization models based on Modern Portfolio Theory are due to their sensitivity to errors in return estimates or correlations.

But we will discuss this relationship between stocks and bonds in the article “The 60/40 portfolio”, how this relationship has changed in recent months and what is expected in the future.

Regarding the elimination of specific risk, the combination of assets in a portfolio should reduce the volatility of the portfolio. However, this approach does not necessarily result in fall protection or eliminate all risks.

Another criticism pointed out is that the MPT evaluates portfolios based on variance and not on the risk of falling. For example, two hypothetical portfolios that have the same level of variance and returns are considered similar in modern portfolio theory. However, one portfolio may have this variance due to frequent small losses, while the other may have experienced some large declines.

How to calculate risk and return according to MPT?

Portfolio theory is based on the principle that investment opportunities can be evaluated through the expected return and the variance of the return, as a measure of risk.

The expected return is often confused with the return verified in the past. Of course, we shouldn't project past returns into the future, but simplification and easiness can lead us to make this mistake.

There are also some interesting shortcuts like projecting the standard deviation, which becomes much more stable in terms of the forecast and estimating the return as 60% of the standard deviation. This technique allows us to think objectively, that is, the investor or manager intends to transform part of the volatility assumed in the portfolio into a return.

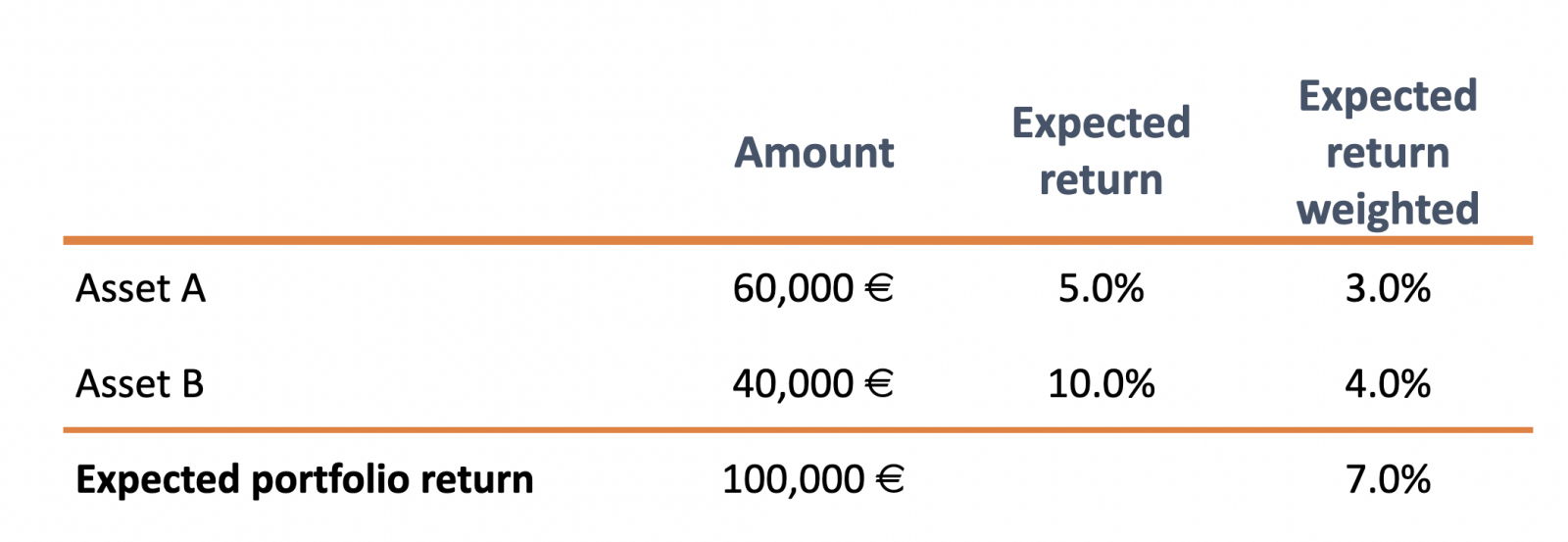

But let's take a concrete example:

Consider a portfolio of €100,000 composed of two assets:

MPT has underlying, as we have already mentioned, mathematical concepts for the asset allocation process. Investors must multiply the percentage weight that each asset occupies in the portfolio by the level of volatility or return it is expected to deliver. Then it must sum the adjusted risk levels weighted to the total risk of the portfolio and the adjusted expected returns weighted to the expected return of the portfolio.

The easiest way to create a diversified portfolio is to buy combinations between asset classes and investments that are not positively correlated.

MPT - Variations and Alternatives

Naturally, this theory led to the emergence of many others, such as the APT (Arbitrage pricing theory) and the PMPT (Post-Modern Portfolio Theory). Both try to overcome some of the disadvantages of MPT and bring new readings of the way we invest and how we should invest. APT brings, for example, macroeconomic factors into the equation of estimating asset value and PMPT seeks to overcome the disadvantage of MPT not considering downside risk.

In response to the problem of forecast errors in returns and correlations, practitioners have developed an investment approach in which asset classes are weighted according to the contribution of risk. This approach is known as risk-parity.

In the 90s of the last century and in the beginning of this century, the links between behavioural factors and the construction of the portfolio emerged. Shefrin and Statman developed the Behavioral Portfolio Theory by trying to reflect how investors actually build portfolios, rather than how traditional theory suggests they do.

Conclusion

Whether you use a financial advisor or invest independently, it is important to know how this investment strategy works. Understand, for example, the reason for diversification and its effects when we combine assets with different correlations between them. Always starting from our personal goals, we cannot forget that our portfolio is unique, it belongs to no one else. It is adapted to our current and projected reality. The combination of the theoretical basis and individual reality should result in a fully optimized and personalized portfolio, adjusted to objective return, risk tolerance and investor preferences and restrictions.

We want to help you be a better investor:

- We help you develop your Investment Policy Statement;

- We develop individual or group training on investments and savings;

- We quantitatively analyze your current portfolio with Future Analyzer's computational technology and finances;

- Request more information about the investment advisory service provided through Banco Invest.

Vítor is a CFA® charterholder, entrepreneur, music lover and with a dream of building a true investment and financial planning ecosystem at the service of families and organizations.

+351 939873441 (Vítor Mário Ribeiro, CFA)

+351 938438594 (Luís Silva)

Future Proof is an Appointed Representative of Banco Invest, S.A.. It is registered at CMVM.